It looks like you're using an Ad Blocker.

Please white-list or disable AboveTopSecret.com in your ad-blocking tool.

Thank you.

Some features of ATS will be disabled while you continue to use an ad-blocker.

-@TH3WH17ERABB17- -Q- Questions ---ASCENSION--- -Part- --43--

page: 79share:

a reply to: Thoughtful2

I've not seen the Mr Pool golden circle post - do you have a copy you can post so I can archive it? Pretty please!

GOLDEN CIRCLE is a signpost to KINGSMAN: THE GOLDEN CIRCLE, where the evil Poppy has laced drugs worldwide with a lethal disease and blackmails the government for release of the prepared cure!

We've covered the film in the thread before!

I think this is pointing to the triggering of the Marburg virus capsules already in the vaccinated from the covid jab!

I've not seen the Mr Pool golden circle post - do you have a copy you can post so I can archive it? Pretty please!

GOLDEN CIRCLE is a signpost to KINGSMAN: THE GOLDEN CIRCLE, where the evil Poppy has laced drugs worldwide with a lethal disease and blackmails the government for release of the prepared cure!

We've covered the film in the thread before!

I think this is pointing to the triggering of the Marburg virus capsules already in the vaccinated from the covid jab!

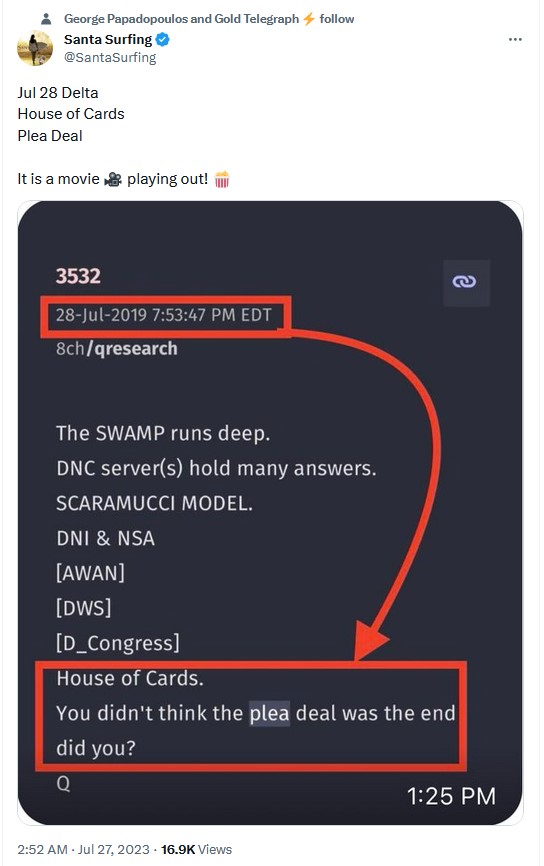

Thanks to Santa Surfing for this forewarning of a 4 yr DELTA on Friday

28th of #3532:

So now we see that the failure of Hunter Biden's plea deal is key to the collapse of the HOUSE OF CARDS.

Also think of a HOUSE OF CARDS as each layer being a generation of the Biden family?

So now we see that the failure of Hunter Biden's plea deal is key to the collapse of the HOUSE OF CARDS.

Also think of a HOUSE OF CARDS as each layer being a generation of the Biden family?

Nothing to see here folks. Usual tax evasion stuff, like Trump proudly owned that he did the same, kept as much of his money from the government as he

was able. And so did Hunter Biden, same strategy because your government laws allow the rich to pay nadda. Its your fault hard working people, you

allow this to happen and just whine and do nothing.

originally posted by: RelSciHistItSufi

a reply to: Guyfriday

You were in college in the Middle Ages???

I jest!

Where do you think I earned my pileus quadratus, and my penchant for drinking, gambling and prostitutes?

a reply to: RelSciHistItSufi

House of Cards you say?

From: ABC News

Actor Kevin Spacey was on Wednesday found not guilty in a London court of a series of sexual assaults against several accusers.

Twelve jurors at the Southwark Crown Court had begun deliberating at about noon on Monday following a three-week trial. Spacey, 64, had pleaded not guilty to 12 charges of sexual assault.

The jury cleared Spacey of nine charges. The additional charges had been struck down before the jury began its deliberations.

Prosecutors had sought during the trial to label Spacey as a "sexual bully," and the actor took the stand to defend himself. Musician Elton John appeared as a witness for the defense, testifying remotely from Monaco about Spacey once attending a gala at his Windsor home.

He was the lead on "House of Cards", so I wonder?

originally posted by: queenofswords

a reply to: FlyingFox

Biden will pardon him before it comes down to conviction, imo, and be damned the people who object to it. This is the way they roll.

There's a reason they haven't played that card.

It might not even be available to them.

a reply to: FlyingFox

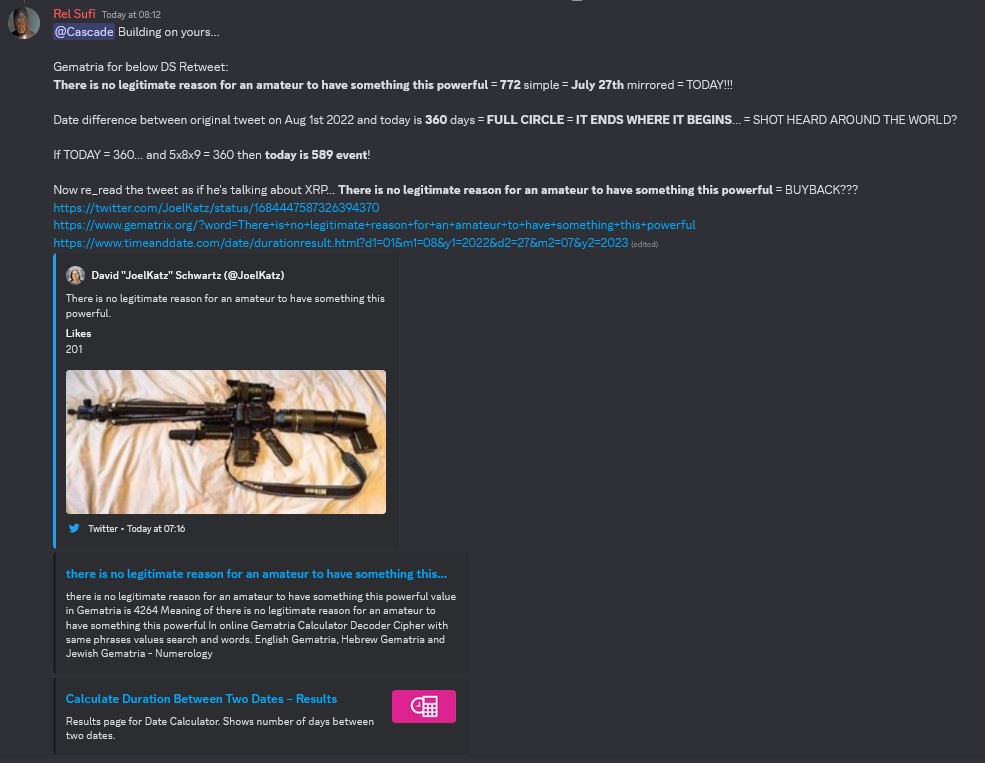

Well Q posted "(2 days ahead of schedule)" on Jan 5th, 2019 in #2644. ...which includes this Donald Trump tweet:

Hebrew Gematria for:

The Democrats want Billions of Dollars for Foreign Aid, but they don’t want to spend a small fraction of that number on properly securing our Border = 7727 ... Today, July 27th?

In English gematria = 8808

Gematria equivalents for: FIGURE THAT ONE OUT =

DIGITAL CURRENCY,

AND THEN SUDDENLY,

ELEVATOR

(All tie to Mr Pool posts!)

Of interest that Basel III capital balance sheet requirements become effective today... so we may see stock market crash as a result of numerous banks going bankrupt?

Anywho... The point I was going to make is that, just because we were 2 days ahead of schedule at the start of 2019 doesn't mean we still are now?

Well Q posted "(2 days ahead of schedule)" on Jan 5th, 2019 in #2644. ...which includes this Donald Trump tweet:

The Democrats want Billions of Dollars for Foreign Aid, but they don’t want to spend a small fraction of that number on properly securing our Border. Figure that one out!

Hebrew Gematria for:

The Democrats want Billions of Dollars for Foreign Aid, but they don’t want to spend a small fraction of that number on properly securing our Border = 7727 ... Today, July 27th?

In English gematria = 8808

Gematria equivalents for: FIGURE THAT ONE OUT =

DIGITAL CURRENCY,

AND THEN SUDDENLY,

ELEVATOR

(All tie to Mr Pool posts!)

Of interest that Basel III capital balance sheet requirements become effective today... so we may see stock market crash as a result of numerous banks going bankrupt?

Anywho... The point I was going to make is that, just because we were 2 days ahead of schedule at the start of 2019 doesn't mean we still are now?

edit on 27-7-2023 by RelSciHistItSufi because: (no reason given)

a reply to: RelSciHistItSufi

There is more Pope news.

Portuguese Sex Abuse Scandal

This isn't just a handful of cases and has been going on for a long time. What is so disturbing is how they have done as much as possible to avoid responsibility and accountability.

They have had to walk back some of the more ludicrous positions such as claiming that reparations would be insulting to the victim.

#1950

House of God?

Only the beginning.

Those who you are taught to trust are the most....

Expect MANY, MANY, MANY similar reports to surface from around the world.

IT GOES A LOT DEEPER.

Connected.

The choice to know will be yours.

Wealth?

Power?

Sanctuary against criminal prosecution?

Recipe for........

I imagine the timing of this couldn't be worse for the Pope.

There is more Pope news.

Portuguese Sex Abuse Scandal

This isn't just a handful of cases and has been going on for a long time. What is so disturbing is how they have done as much as possible to avoid responsibility and accountability.

They have had to walk back some of the more ludicrous positions such as claiming that reparations would be insulting to the victim.

#1950

House of God?

Only the beginning.

Those who you are taught to trust are the most....

Expect MANY, MANY, MANY similar reports to surface from around the world.

IT GOES A LOT DEEPER.

Connected.

The choice to know will be yours.

Wealth?

Power?

Sanctuary against criminal prosecution?

Recipe for........

I imagine the timing of this couldn't be worse for the Pope.

a reply to: RelSciHistItSufi

Thankyou RelSciHistItSufi for always explaining things and educating us (the masses) in a way that is easy to understand and appreciate!

Thankyou RelSciHistItSufi for always explaining things and educating us (the masses) in a way that is easy to understand and appreciate!

a reply to: RelSciHistItSufi

I'm so sorry Rel I don't have that gold circle Loop post. It was picked up by Fojack twitter a few weeks ago. You may find this difficult to believe but I just memorize them automatically, just like the Q posts. It comes in handy when I am cross referencing all the books I've been reading.

There seems to be a lot of talk about satanic right now.

Glenn Beck Fox News and the satanic temple

#15

This line stands out-

A deep cleaning is occuring and the prevention and DEFENCE Of PURE EVIL is occuring on a daily basis.

[emphasis is mine]

So FOX news is now defending evil?

At the rate they are going they will alienate their remaining audience.

Slap in the Face to Christians

I'm so sorry Rel I don't have that gold circle Loop post. It was picked up by Fojack twitter a few weeks ago. You may find this difficult to believe but I just memorize them automatically, just like the Q posts. It comes in handy when I am cross referencing all the books I've been reading.

There seems to be a lot of talk about satanic right now.

Glenn Beck Fox News and the satanic temple

#15

This line stands out-

A deep cleaning is occuring and the prevention and DEFENCE Of PURE EVIL is occuring on a daily basis.

[emphasis is mine]

So FOX news is now defending evil?

At the rate they are going they will alienate their remaining audience.

Slap in the Face to Christians

Fed approves hike that takes interest rates to highest level in more than 22 years

www.google.com...

PacWest, Banc of California Merge to Get Smaller. Others May Follow.

PacWest Bank, Thrashed by Deposit Crisis, Will Be Taken Over

www.nytimes.com...

JPMorgan to buy almost $2 billion of mortgages in the PacWest deal, source says

www.reuters.com...

NO ACCESS Chase down updates — Hundreds of Zelle users unable to access bank deposits as issue addressed

www.the-sun.com...

Uninsured depositors remain a ticking time bomb for the U.S. banking system

www.google.com...

US regulator accuses banks of misreporting deposit data

www.ft.com...

Big US Banks Gird for New Capital Rules Coming Tomorrow

www.bloomberg.com...

Attorneys general say FDIC bailout of failed banks will harm taxpayers

www.google.com...

A severe recession is on the horizon - and the Fed will axe interest rates to limit the fallout, DoubleLine's chief investor says

www.businessinsider.com...

"I would say it's certainly possible that we will raise funds again at the September meeting if the data warranted," said Powell. "And I would also say it's possible that we would choose to hold steady and we're going to be making careful assessments, as I said, meeting by meeting."

www.google.com...

PacWest, Banc of California Merge to Get Smaller. Others May Follow.

PacWest Bank, Thrashed by Deposit Crisis, Will Be Taken Over

The merger marks a rare transaction in the market after several months of government-negotiated sales of failed banks. Bank mergers have also been held up for months or scrapped awaiting regulatory approval.

www.nytimes.com...

JPMorgan to buy almost $2 billion of mortgages in the PacWest deal, source says

JPMorgan Chase & Co will buy almost $2 billion worth of mortgages to facilitate Banc of California's purchase of PacWest Bancorp (PACW.O), a source with knowledge of the matter told Reuters.

The investment bank has entered into an agreement to buy $1.8 billion of single-family residential loans at a discount, the source said.

www.reuters.com...

NO ACCESS Chase down updates — Hundreds of Zelle users unable to access bank deposits as issue addressed

HUNDREDS of Zelle and Chase users were unable to access their direct deposits on Tuesday.

www.the-sun.com...

Uninsured depositors remain a ticking time bomb for the U.S. banking system

The failures of three sizable banks in March and April exposed major weaknesses in bank regulation. Who did what to whom, and when–a favorite Washington game–is currently playing out. What has received less attention is the major role that uninsured depositors played in these bank failures–and how uninsured deposits remain a major source of instability for the U.S. banking system.

www.google.com...

US regulator accuses banks of misreporting deposit data

A top US banking regulator has accused some US lenders of misreporting deposit data at a time of industry tension over how deposit levels will be used to assess the cost of this year’s failures of Silicon Valley Bank and Signature Bank.

www.ft.com...

Big US Banks Gird for New Capital Rules Coming Tomorrow

Wall Street’s biggest banks are bracing for impact.

New rules coming tomorrow could eat up almost all the excess capital they’ve tucked away over the past decade by forcing lenders to thicken their financial cushions — as much as an extra two percentage points of capital — to absorb unexpected losses.

www.bloomberg.com...

Attorneys general say FDIC bailout of failed banks will harm taxpayers

The FDIC announced earlier this year $15.8 billion split between the banks would cover 95% of the costs of uninsured deposits from Silicon Valley Bank and Signature Bank. The financial agency took over the two banks in March after they failed

No matter how well intentioned the Federal Government's actions may be, it cannot guarantee that 'no losses will be borne by the taxpayer,'" the attorneys general said in their letter. "The special assessment may not be directly levied against them, but those costs will ultimately be passed on to taxpayers."

www.google.com...

A severe recession is on the horizon - and the Fed will axe interest rates to limit the fallout, DoubleLine's chief investor says

The US economy will suffer a severe recession, spurring the Federal Reserve to slash interest rates by a whole percentage point at once, DoubleLine Capital's chief investment officer says.

www.businessinsider.com...

a reply to: Guyfriday

What a surprise-

Campai gn Finance Charges Dropped Against Sam Bankman Fried

Aside from the political donations half of the donations went to Protect our Future PAC- Pandemic preparedness. Odd how that was slipped in.

A few words from the World Bank-

Pandemic Fund Allocates First Grants

"The demand from countries for grant financing to strengthen pandemic prevention, preparedness and response is clear-the first call for proposals was 8 times oversubscribed.'

No doubt something is being prepared for us.

What a surprise-

Campai gn Finance Charges Dropped Against Sam Bankman Fried

Aside from the political donations half of the donations went to Protect our Future PAC- Pandemic preparedness. Odd how that was slipped in.

A few words from the World Bank-

Pandemic Fund Allocates First Grants

"The demand from countries for grant financing to strengthen pandemic prevention, preparedness and response is clear-the first call for proposals was 8 times oversubscribed.'

No doubt something is being prepared for us.

a reply to: FlyingFox

One more thing as a result of the stolen election-

Project Veritas

Disturbing... the CCP made a new 5 year plan right after Biden was placed as President. Bill Gates probably knows the details since he is BF with Xi.

Some Details

This is just the tip of the iceberg.

One more thing as a result of the stolen election-

Project Veritas

Disturbing... the CCP made a new 5 year plan right after Biden was placed as President. Bill Gates probably knows the details since he is BF with Xi.

Some Details

This is just the tip of the iceberg.

EU Banks See Record Collapse In Loan Demand

www.zerohedge.com...

Europe’s banks are bracing for a wave of defaults

amp.cnn.com...

European banks flag bad loan risks as global economy falters

www.reuters.com...

Factbox: European companies cut jobs as economy sputters

www.reuters.com...

Europeans Are Becoming Poorer. ‘Yes, We’re All Worse Off.’

www.wsj.com...

Europe’s economic engine is stalling: Germany deindustrializes

www.google.com...

In its quarterly survey of 158 big banks, the European Central Bank (ECB) said that demand for loans from businesses over the last three months fell at the fastest pace on record (the time series began in 2003) and banks tightened their credit standard to consumers over the last three months.

Demand for mortgages also dropped sharply, though not as much as the "very large" decrease in the previous two quarters, but a further moderate drop is likely during the third quarter, the ECB added.

Banks said that their stock of non-performing loans (NPL) also pushed them to tighten credit standards.

www.zerohedge.com...

Europe’s banks are bracing for a wave of defaults

Some of Europe’s biggest banks are setting aside more cash to absorb potential losses on loans, as rising interest rates increase pressure on borrowers.

amp.cnn.com...

European banks flag bad loan risks as global economy falters

The latest flurry of bank earnings in Europe highlighted broader trends in global banking, where investment banks are under pressure due to a deal drought, while higher interest rates are helping profitability in retail banking.

www.reuters.com...

Factbox: European companies cut jobs as economy sputters

Decades-high inflation and the impact of war in Ukraine have forced companies across Europe into lay-offs or hiring freezes.

www.reuters.com...

Europeans Are Becoming Poorer. ‘Yes, We’re All Worse Off.’

Europeans are facing a new economic reality, one they haven’t experienced in decades. They are becoming poorer.

www.wsj.com...

Europe’s economic engine is stalling: Germany deindustrializes

Suddenly, a perfect storm is brewing over the former European powerhouse, signaling that its current recession isn’t just “technical,” as policymakers pray, but rather a harbinger of a fundamental reversal in economic fortunes that threatens to send tremors across Europe, injecting even more upheaval into the Continent’s already polarized political landscape.

www.google.com...

a reply to: socialmediaclown

Wow that is big news. Thank you for covering all of this.

Biden Family Scandals

The media has been overly focused on the raunchy side of Hunter but there is much more around this.

"Not only did the intelligence agencies interfere with the 2020 election, but in their efforts to protect Joe Biden, they likely also failed to provide necessary defensive briefings putting Americans at risk.

To date, this scandal has been over-looked and merits further inquiry to determine whether the intelligence apparatus fufilled its duty to the country or omitted inconvenient facts in briefings to protect Joe Biden."

If they omit these facts what other facts have they omitted over other issues. They get to cherry pick whatever fits their agenda. Clearly these intelligence agencies are not to be trusted. In fact they probably are doing the same thing to Biden.

Wow that is big news. Thank you for covering all of this.

Biden Family Scandals

The media has been overly focused on the raunchy side of Hunter but there is much more around this.

"Not only did the intelligence agencies interfere with the 2020 election, but in their efforts to protect Joe Biden, they likely also failed to provide necessary defensive briefings putting Americans at risk.

To date, this scandal has been over-looked and merits further inquiry to determine whether the intelligence apparatus fufilled its duty to the country or omitted inconvenient facts in briefings to protect Joe Biden."

If they omit these facts what other facts have they omitted over other issues. They get to cherry pick whatever fits their agenda. Clearly these intelligence agencies are not to be trusted. In fact they probably are doing the same thing to Biden.

J.P. Morgan Exec Referred to Epstein's Teen Girls as 'Nymphettes' in Newly Surfaced Email

jezebel.com...

JP Morgan execs face new allegations from U.S. Virgin Islands in $190 million Jeffrey Epstein lawsuit

www.google.com...

New and nauseating accusations have been made in the ongoing litigation between the U.S. Virgin Islands and J.P. Morgan over their respective relationships with Jeffrey Epstein. That’s right; the battle royale between the mega bank and the sandbox for the obscenely wealthy continues and somehow has become more revolting.

In new court filings on Monday, the U.S. Virgin Islands—where the deceased sex-trafficker and pedophile maintained a residence—accused J.P. Morgan of turning a blind eye to Epstein’s criminal activities in its 15-year relationship with him. Among the most eyebrow-raising inclusions in the Virgin Islands’ documents were emails demonstrating just how close some executives were to Epstein.

In one September 2012 email from a senior J.P. Morgan executive to Mary Erdoes, the bank’s CEO for asset and wealth management, they compared a client’s home to Epstein’s: “Reminded me of JE’s house, except it was more tasteful, and fewer nymphettes,” the exec wrote. “More like the Frick [museum]. Art was fabulous.” Apparently, “nymphettes” is rich ghoul code for underage girl. Who knew!

jezebel.com...

JP Morgan execs face new allegations from U.S. Virgin Islands in $190 million Jeffrey Epstein lawsuit

The government of the U.S. Virgin Islands unveiled fresh allegations against JP Morgan Chase this week over its ties to the disgraced late financier Jeffrey Epstein. It's part of a massive lawsuit that accuses the bank of helping conceal his sex crimes and seeks at least $190 million. A lengthy series of new court filings detail the bank's alleged dealings with Epstein while he was a client between 1998 and 2013.

www.google.com...

new topics

-

Don't cry do Cryo instead

General Chit Chat: 4 hours ago -

Tariffs all around, Except for ...

Predictions & Prophecies: 6 hours ago -

Gen Flynn's Sister and her cohort blow the whistle on DHS/CBP involvement in child trafficking.

Whistle Blowers and Leaked Documents: 11 hours ago

top topics

-

Trump sues media outlets -- 10 Billion Dollar lawsuit

US Political Madness: 17 hours ago, 25 flags -

Bucks County commissioners vote to count illegal ballots in Pennsylvania recount

2024 Elections: 16 hours ago, 23 flags -

Fired fema employee speaks.

US Political Madness: 17 hours ago, 10 flags -

Gen Flynn's Sister and her cohort blow the whistle on DHS/CBP involvement in child trafficking.

Whistle Blowers and Leaked Documents: 11 hours ago, 8 flags -

Don't cry do Cryo instead

General Chit Chat: 4 hours ago, 4 flags -

Anybody else using Pomodoro time management technique?

General Chit Chat: 14 hours ago, 3 flags -

Tariffs all around, Except for ...

Predictions & Prophecies: 6 hours ago, 3 flags

active topics

-

Anybody else using Pomodoro time management technique?

General Chit Chat • 8 • : billxam1 -

Tariffs all around, Except for ...

Predictions & Prophecies • 11 • : Dalamax -

How can you defend yourself when the police will not tell you what you did?

Posse Comitatus • 84 • : bastion -

Oligarchy It Is Then

Short Stories • 14 • : UKTruth -

Don't cry do Cryo instead

General Chit Chat • 1 • : angelchemuel -

Mike Tyson returns 11-15-24

World Sports • 54 • : angelchemuel -

President-Elect DONALD TRUMP's 2nd-Term Administration Takes Shape.

Political Ideology • 205 • : WeMustCare -

On Nov. 5th 2024 - AMERICANS Prevented the Complete Destruction of America from Within.

2024 Elections • 155 • : WeMustCare -

The Trump effect 6 days after 2024 election

2024 Elections • 143 • : cherokeetroy -

Bucks County commissioners vote to count illegal ballots in Pennsylvania recount

2024 Elections • 21 • : Irishhaf